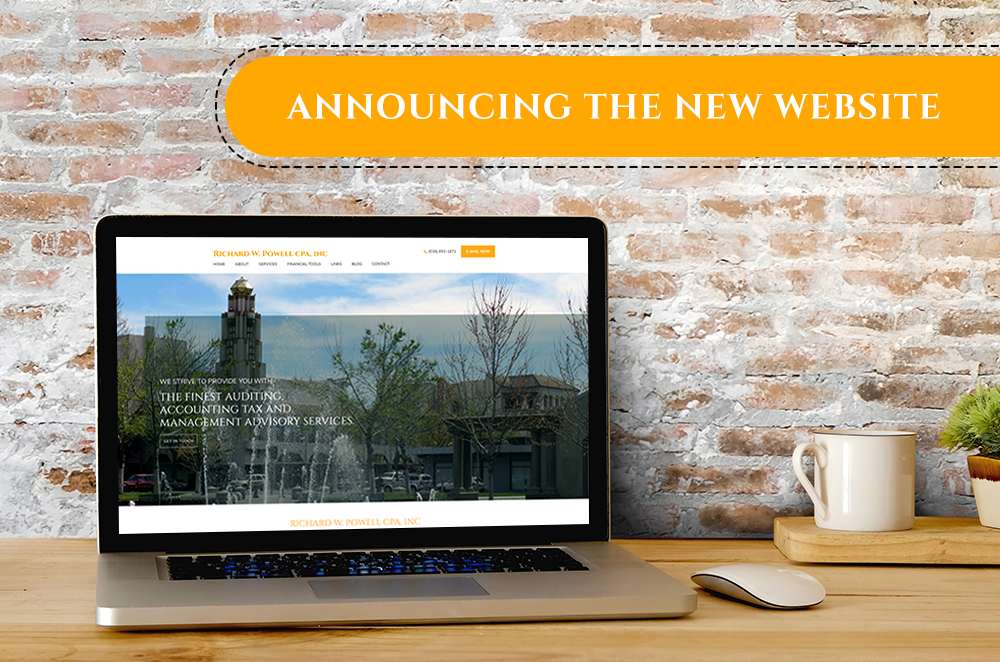

We are delighted to announce the launch of our new website!

-

Announcing The New Website

CLICK HERE TO READ THE FULL ARTICLE »

-

New Website Under Construction

New Website Coming Soon!

CLICK HERE TO READ THE FULL ARTICLE »

-

IRS Releases 2021 Inflation-Adjusted Tax Tables, Standard Deduction, AMT and Other Amounts

The IRS has released the annual inflation adjustments for 2021 for the income tax rate tables, and for over 50 other tax provisions. The IRS makes these cost-of-living adjustments (COLAs) each year to reflect inflation. 2021 Income Tax Brackets For 2021, the highest income tax bracket of 37 percent applies when taxable income hits: $628,300 for married individuals filing jointly and surviving spouses, $523,600 for single individuals and heads of households, $314,150 for married individuals filing separately, and $13,050 for estates and trusts. 2021 Standard Deduction The standard deduction for 2021 is: $25,100 for married individuals filing jointly and surviving spouses, $18,800 for heads of households, and $12,550 for single individuals…

CLICK HERE TO READ THE FULL ARTICLE »

-

2021 Inflation Adjustments for Pension Plans, Retirement Accounts Released

The IRS has released the 2021 cost-of-living adjustments (COLAs) for pension plan dollar limitations and other retirement-related provisions. Key Unchanged Amounts The 2021 contribution limit remains unchanged at $19,500 for employees who take part in: 401(k) plans, 403(b) plans, most 457 plans, and the federal government’s Thrift Savings Plan The catch-up contribution limit for employees aged 50 and over who participate in these plans also remains unchanged at $6,500. The limitation for SIMPLE retirement accounts is unchanged at $13,500. For individual retirement arrangements (IRAs), the limit on annual contributions to an IRA remains unchanged at $6,000. The additional catch-up contribution limit for individuals aged 50 and over is not…

CLICK HERE TO READ THE FULL ARTICLE »

-

Supreme Court Hears Oral Arguments in ACA Challenge

The U.S. Supreme Court heard oral arguments in California v. Texas, the latest challenge to the Affordable Care Act (ACA). The ACA expanded insurance coverage, and includes popular provisions such as required coverage of preexisting medical conditions. Three major issues are at play in this case: Do the plaintiff challengers of ACA—two individuals, the Trump Administration, and a number of states led by Texas—have standing to bring this case? Did reducing the penalty amount under Code Sec. 5000A(c) to $0 render the individual mandate in the ACA unconstitutional? If the mandate is unconstitutional, does that mean the act itself is unconstitutional, in whole or in part? Background The individual…

CLICK HERE TO READ THE FULL ARTICLE »

-

Guidance for Applying New, Proposed Bonus Depreciations Regs

The IRS has provided guidance to taxpayers that want to apply either Reg. §1.168(k)-2 and Reg. §1.1502-68, or want to rely on proposed regulations under NPRM REG-106808-19, for: certain depreciable property acquired and placed in service after September 27, 2017, by the taxpayer during its tax years ending on or after September 28, 2017, and before the taxpayer's first tax year that begins on or after January 1, 2021; certain plants planted or grafted after September 27, 2017, by the taxpayer during its tax years ending on or after September 28, 2017, and before the taxpayer's first tax year that begins on or after January 1,…

CLICK HERE TO READ THE FULL ARTICLE »

-

Guidance on Form W-2 Reporting of Deferred Employee Tax

The IRS has released guidance on its website for employers and employees regarding deferral of employee Social Security tax under Notice 2020-65, I.R.B. 2020-38, 567. In August, the IRS issued Notice 2020-65 in response to a Presidential Memorandum that allowed deferral of the withholding, deposit, and payment of certain employee payroll tax obligations. The Notice allows employers the option to defer the employee portion of Social Security tax from September 1, 2020, through December 31, 2020, for eligible employees who earn less than $4,000 per bi-weekly pay period (or the equivalent threshold amount with respect to other pay periods) on a pay period-by-pay period…

CLICK HERE TO READ THE FULL ARTICLE »

-

Life Expectancy and Distribution Period Tables for RMDs Updated

The IRS has issued final regulations to update the life expectancy and distribution period tables under the required minimum distribution (RMD) rules. The tables reflect the general increase in life expectancy. The tables would apply for distribution calendar years beginning on or after January 1, 2022, with transition relief. RMDs apply to qualified plans, including 401(k) plans and profit sharing plans. They also apply to IRAs (including SEP and SIMPLE IRAs), inherited Roth IRAs, Tax Sheltered Annuity plans, and eligible deferred compensation plans. In general, RMDs must begin for the year the individual reaches age 72. An RMD for a calendar…

CLICK HERE TO READ THE FULL ARTICLE »

-

Proposed Regs Address State and Local Tax Payments by Partnerships, S Corporations

The IRS intends to issue proposed regulations to clarify that state and local income taxes imposed on and paid by a partnership or an S corporation are deductible by the partnership or S corporation in computing non-separately stated taxable income for the year of the payment. The proposed regulations are intended to provide certainty to individual partners and S corporation shareholders in calculating their state and local tax (SALT) deduction limitations. The proposed regs described in the notice apply to specified income tax payments made on or after November 9, 2020. Taxpayers can also apply these rules to specified income tax…

CLICK HERE TO READ THE FULL ARTICLE »